In recent years, the National Pension System (NPS) has become the go-to retirement savings option for lakhs of employees in India, especially in government and banking sectors. But behind the promise of secure post-retirement life lies a growing concern for thousands of public sector bank employees—they are stuck with rigid investment rules and no say in how their pension money is managed.

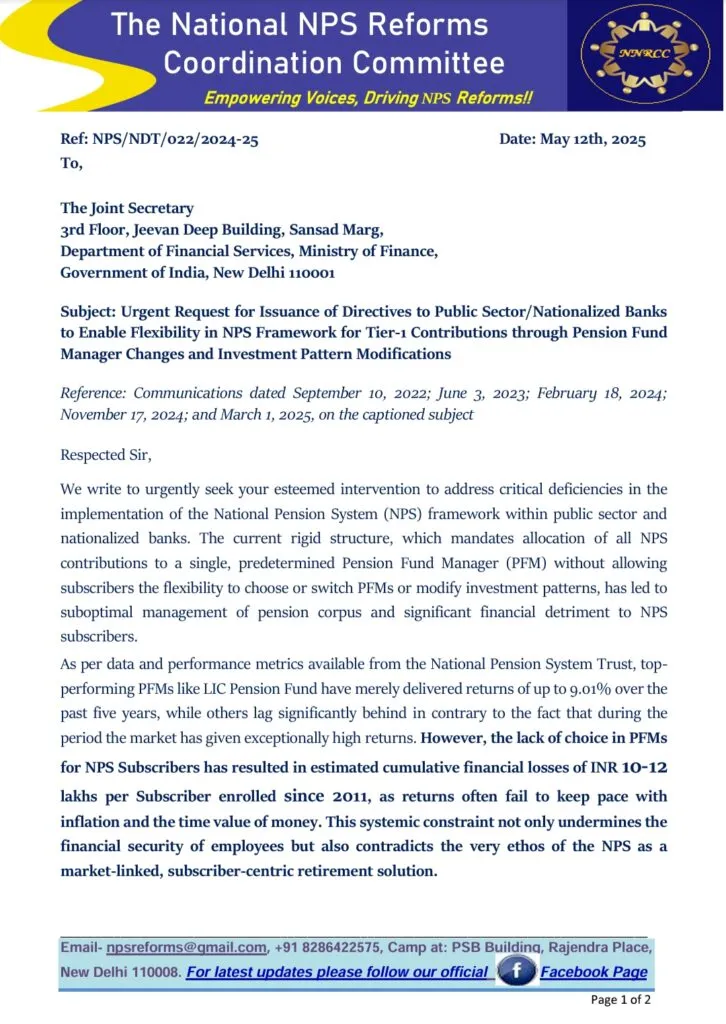

Recently, the National NPS Reforms Coordination Committee (NNRCC) took a bold step. On May 12, 2025, they submitted a formal letter to the Ministry of Finance, highlighting critical flaws in how NPS is implemented in public sector banks.

What’s the Problem with NPS in Banks?

If you’re a bank employee under NPS, you might already know this:

- You cannot choose which Pension Fund Manager (PFM) manages your retirement money.

- You can’t switch PFMs, even if another one gives better returns.

- You are not allowed to modify your investment pattern (equity, debt, government securities, etc.).

This means your hard-earned pension money is locked into a system where you have no control, even though it’s your future that depends on it.

According to NNRCC, this lack of choice has cost many employees heavily. In fact, they estimate a loss of Rs. 10–12 lakh per subscriber who joined NPS since 2011, due to low returns compared to market performance.

But Isn’t NPS Supposed to Be Flexible?

Yes, it is. The Pension Fund Regulatory and Development Authority (PFRDA) has clear guidelines that allow subscribers to:

- Choose and switch PFMs

- Modify their investment allocation (for example, put more in equity or debt)

Unfortunately, these options exist only on paper for many bank employees, as most public sector and nationalized banks haven’t enabled these features.

What Central Government Employees Get (That Bank Staff Don’t)

There’s a big gap in treatment.

Central Government employees who joined NPS after April 1, 2019, can:

- Choose their Pension Fund Manager

- Change their investment preferences anytime

But bank employees under the same NPS framework?

They’re still stuck with a one-size-fits-all model, often losing out on better returns.

What the Committee is Demanding

The NNRCC has made three clear demands to the Ministry of Finance:

- Allow PFM Choice:

Let bank employees choose and switch their Pension Fund Manager to maximize returns. - Enable Investment Flexibility:

Allow them to choose how their NPS Tier-1 money is invested – equity, government bonds, or auto-choice – just like other subscribers. - Set Up NPS Advisory Cells in Banks:

Each bank should create a support unit to:- Monitor fund performance

- Educate employees on investment options

- Offer retirement planning support

Why These Changes Matter

This isn’t just about better returns. It’s about fairness, financial security, and the right to control your own future.

Thousands of public sector bank employees are working hard every day, yet they don’t have basic investment freedoms under NPS. Fixing this gap can:

- Increase trust in the system

- Improve employee satisfaction

- Ensure more efficient use of retirement savings

The NPS is meant to empower individuals to build their financial future. But if the system blocks flexibility and transparency, it fails the very people it was meant to protect.

The letter sent by the National NPS Reforms Coordination Committee is a strong and timely reminder that reforms are long overdue.

Let’s hope the Ministry listens—and acts—before more bank employees lose out on the returns they rightfully deserve.