The banking in India has changed a lot. Today, Banks remain open till late evening but before liberalisation, the situation was different. For decades, banking in India followed a simple and predictable pattern. The system was highly regulated, competition was limited, and innovation was slow. Bank employees even joked about a phrase that perfectly described the working style of that era — the “4–6–4 rule.”

It meant:

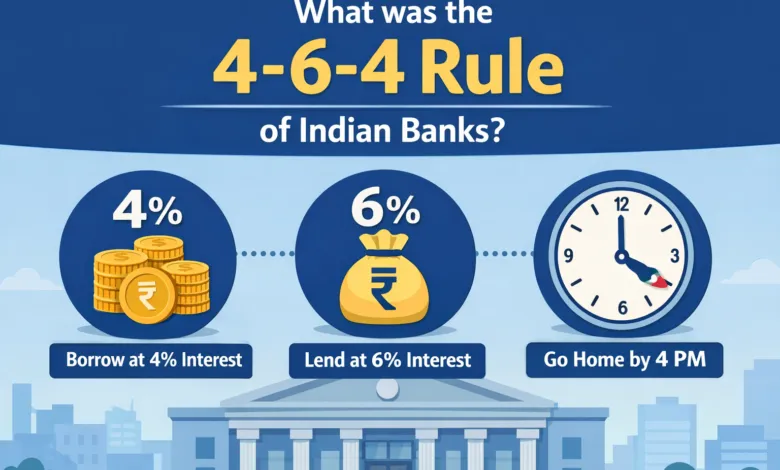

- Borrow money at 4% interest

- Lend it at 6% interest

- Go home by 4 PM

While humorous, the phrase captured the reality of Indian banking before the 1990s. Banks operated in a safe and controlled environment where profitability was steady, risks were minimal, and customer service was not a major focus. Most processes were manual, paperwork was heavy, and banking transactions often took hours—or even days—to complete. But everything began to change with the economic liberalisation reforms of the 1990s. The 4-6-4 Rule consisted of three main components:

1. The 4% Deposit Rate

The rule began with the practice of offering depositors a fixed 4% interest rate on their savings accounts. Because interest rates were strictly regulated by the Reserve Bank of India (RBI), there was virtually no competition between banks for deposits. Everyone received the same low return on their savings.

2. The 6% Lending Rate

Conversely, the lending part of the rule involved charging a fixed 6% interest rate on loans. Again, because rates were non-negotiable and dictated by central policy, all borrowers, from individuals to large corporations, faced the same borrowing cost.

3. The 4 PM Closure

The final part of the rule referred to the typical operating hours of banks. Banks would traditionally close their doors to public transactions by 4 PM. This reflected a less customer-centric approach, where banking hours were set largely for administrative convenience rather than accessibility.

💡 Did You Know? Interesting Facts About Banking in India

- India’s central bank, the Reserve Bank of India (RBI), was established in 1935 and nationalised in 1949.

- The State Bank of India (SBI) is the largest bank in India and traces its origin to the Bank of Calcutta established in 1806.

- India has one of the largest banking networks in the world, with thousands of bank branches and ATMs across the country.

- In 1969, the Government of India nationalised 14 major banks to expand banking services to rural and poor communities.

- The rise of digital banking, UPI, and mobile apps has made India one of the fastest-growing digital payment markets in the world.

- Millions of Indians now use internet banking, mobile banking, and instant payment systems for everyday financial transactions.

The Context and Transition

The 4-6-4 Rule emerged in an era where the primary focus of the nationalized banking sector was on stability and directed credit to priority sectors, rather than profitability or efficiency. The net interest margin—the difference between the lending rate and the deposit rate (a modest 2% in this simplified model)—was enough to cover operational costs in an environment with little innovation and few product offerings.

Before the 1991 economic reforms, India’s banking sector was highly regulated by the government. Most banks were public sector banks, services were limited, and banking operations were mostly manual. Customers often faced slow services, long waiting times, and had very few banking options.

After the liberalisation reforms of the 1990s, the banking sector changed significantly. Private banks entered the market, competition increased, and banks started adopting modern technologies such as ATMs, computerised systems, internet banking, and mobile banking.

As a result, banking services became faster, more efficient, and more customer-friendly, allowing people to perform many financial transactions digitally without visiting bank branches.

From Tradition to Transformation

The journey from the old “4–6–4 rule” era to today’s digital banking ecosystem highlights how dramatically India’s financial sector has evolved. What was once a slow, paperwork-heavy system has become a technology-driven, customer-focused industry that supports economic growth, financial inclusion, and innovation. The reforms of the 1990s did more than modernize banks—they fundamentally reshaped how millions of Indians interact with money.