The SBI Annuity Deposit Scheme is a type of fixed deposit where you deposit a lump sum amount only once (for example, ₹5 lakh). Instead of getting your money back at the end of the tenure like in a normal FD, the bank returns your money every month in the form of EMIs.

Each monthly EMI contains two parts:

- Principal – a portion of the amount you deposited.

- Interest – earned on the balance amount that still remains with the bank.

The interest is calculated on the reducing balance (whatever is left after paying each EMI), compounded quarterly but paid monthly.

This scheme converts your one-time deposit into a steady monthly income, just like a pension or annuity.

Let’s Understand this Scheme with the help of an example:

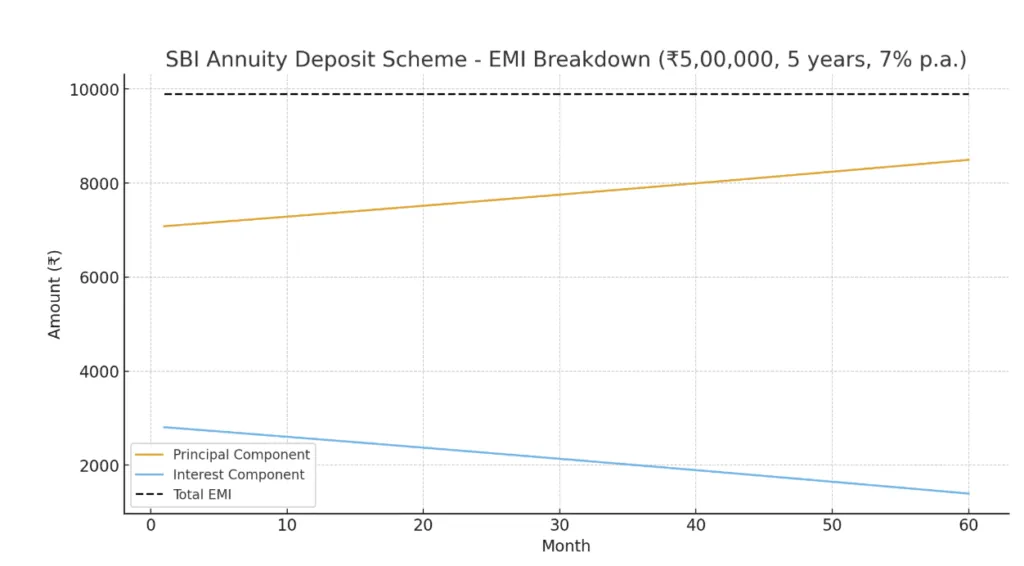

Check the detailed visualization of the SBI Annuity Deposit Scheme (₹5,00,000 for 5 years at 7% p.a.) given below. The black dotted line shows the fixed monthly EMI (~₹9,891). The blue line shows the portion of EMI going towards the principal. The orange line shows the portion of EMI going towards interest, which keeps decreasing as principal reduces.

This demonstrates how, in annuity deposits (similar to loan EMIs), the interest part is higher in the beginning and gradually decreases, while the principal portion increases over time.

Let’s consider one more example and understand the amortization table:

- Deposit (one-time lump sum): ₹1,00,000

- Tenure: 5 years (60 months)

- Interest Rate: 7% per annum (compounded quarterly)

The depositor will receive a fixed monthly EMI that includes both principal + interest. Over time, the interest portion reduces while the principal portion increases (like a loan EMI in reverse).

| Month | EMI (₹) | Interest (₹) | Principal (₹) | Outstanding Principal (₹) |

|---|---|---|---|---|

| 1 | 1,980 | 583 | 1,397 | 98,603 |

| 2 | 1,980 | 576 | 1,404 | 97,199 |

| 3 | 1,980 | 569 | 1,411 | 95,788 |

| 4 | 1,980 | 562 | 1,418 | 94,370 |

| 5 | 1,980 | 555 | 1,425 | 92,945 |

| … | … | … | … | … |

| 56 | 1,980 | 90 | 1,890 | 7,540 |

| 57 | 1,980 | 77 | 1,903 | 5,637 |

| 58 | 1,980 | 64 | 1,916 | 3,721 |

| 59 | 1,980 | 50 | 1,930 | 1,791 |

| 60 | 1,980 | 36 | 1,944 | 0 |

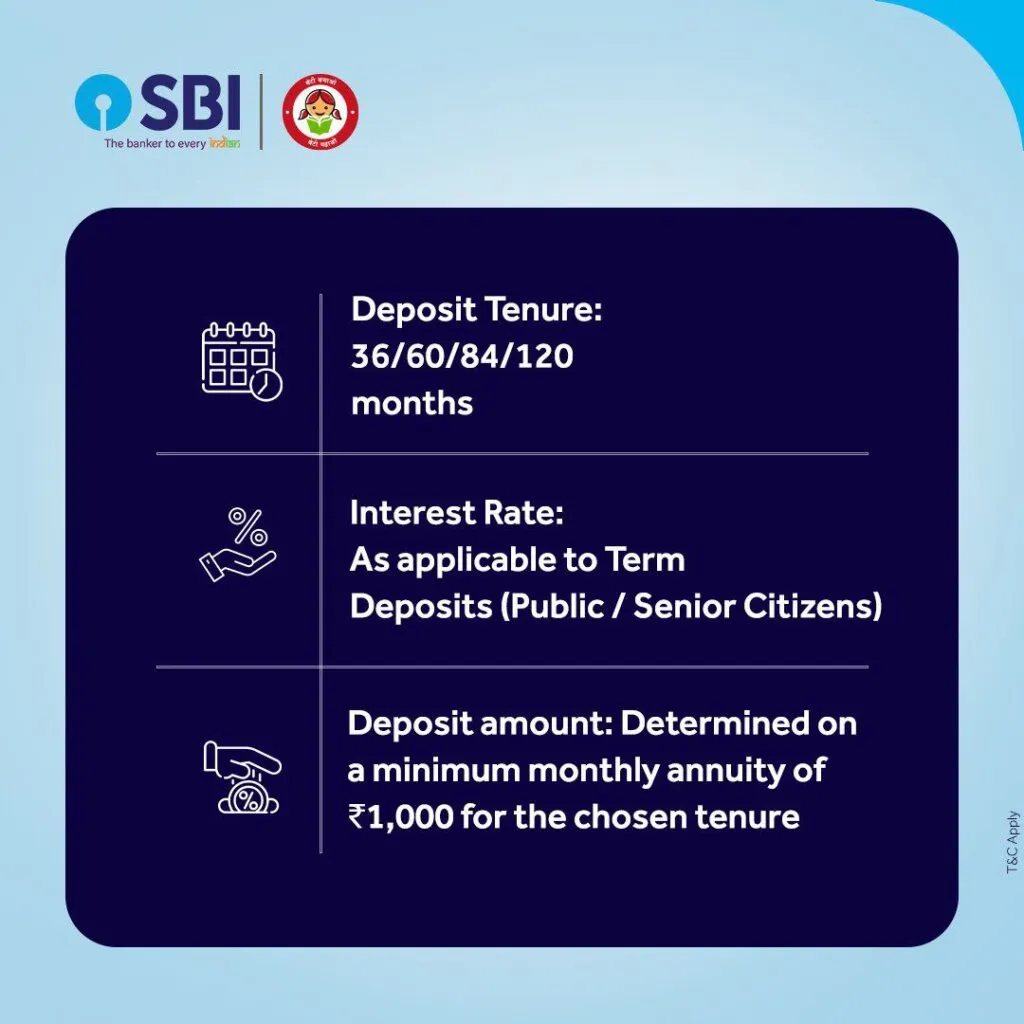

Features of SBI Annuity Deposit Scheme

- To enable the customer to deposit one-time lump sum amount and receive re-payment of the same in monthly annuity instalment comprising part of the principal amount plus interest.

- Period of deposit: 36/60/84 or 120 months

- Available at all branches

- Deposit amount based on minimum monthly annuity of Rs 1000/- for the relevant period

- Premature payment allowed for the deposits up to Rs.15,00,000/-. Penalty chargeable, as applicable to Term Deposits. In case of death of depositor, premature payment is allowed without any limit.

- Maximum deposit amount: No Upper Limit

- Rate of interest as applicable to Term Deposits for Public and Senior Citizens

- Payment of annuity on the anniversary date of the month following the month of deposit.

- If that date is non-existent (29th, 30th & 31st), it will be paid on the 1st day of the next month.

- Nomination is available in favour of individual only

- Overdraft/loan up to 75% of the balance amount of annuity may be granted on special cases.

- After disbursal of OD/loan, further annuity payment will be deposited in loan account only.

- Universal Passbook is issued in lieu of Term Deposit

- Transferability allowed among branches

Can it be termed as a Pension Plan?

The SBI Annuity Deposit Scheme looks like a pension because you invest a lump sum and then receive monthly payments (EMIs). But it is not exactly a pension plan. It’s suitable for people who want regular cash flow after retirement. But duration is limited. Payments stop after the deposit tenure (36, 60, 84, or 120 months) whereas a pension generally continues for lifetime or till spouse’s lifetime.

-

-

-

-

-

-

-

-

-

-

-

-