Good News! Banks will provide compensation upto Rs.25,000 to Customers for Digital Frauds

The Reserve Bank of India (RBI) has introduced a new compensation framework to help customers who suffer losses due to small value fraudulent electronic banking transactions. The rule aims to provide financial relief to genuine victims of online fraud.

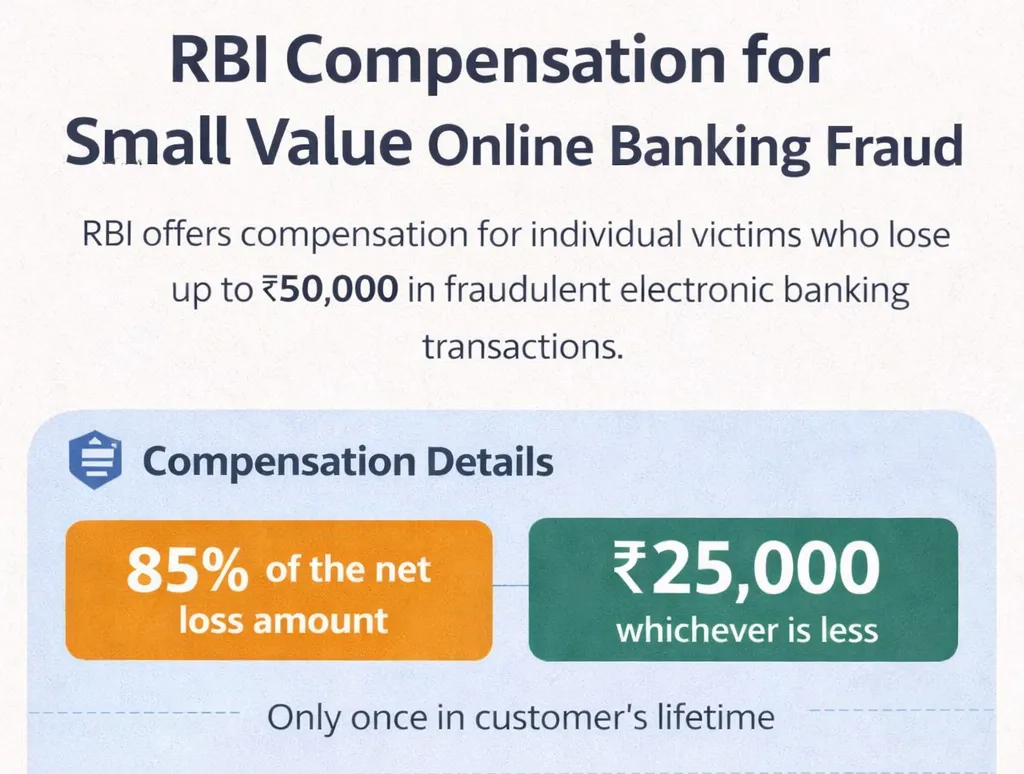

The compensation scheme applies to individual customers who lose up to ₹50,000 due to fraudulent electronic transactions such as unauthorized online transfers or digital banking fraud.

Below are the key details of the new compensation rules.

Compensation Amount for Fraud Victims

If an individual customer becomes a victim of fraudulent electronic banking transactions and files a complaint, the person will receive compensation based on the following rule:

- The customer will receive 85% of the net loss amount, or

- ₹25,000, whichever is lower.

The compensation will be given only once in the customer’s lifetime. The net loss means the total loss after deducting any amount that has already been recovered or returned to the customer.

For example:

- If a customer loses ₹40,000 but ₹15,000 is recovered before compensation, the net loss becomes ₹25,000.

- In this case, compensation will be 85% of ₹25,000, which equals ₹21,250.

Conditions to Receive Compensation

The compensation will be provided only if certain conditions are met.

- The bank must confirm that the loss is genuine and bona fide, according to its internal policies.

- The customer must report the fraud:

- On the National Cyber Crime Reporting Portal, or

- By calling the National Cyber Crime Helpline (1930).

- The fraud must also be reported to the bank within five calendar days of the transaction.

If these conditions are satisfied, the bank will process the compensation claim.

Special Rule for Joint Accounts

If the fraudulent transaction occurs in a joint bank account, only one account holder can claim the compensation.

Once a person claims compensation as a joint account holder, that person cannot claim compensation again in the future as a single account holder, and vice versa.

How the Compensation Amount Is Shared

The compensation amount paid to the customer is shared among three parties:

- Reserve Bank of India

- Customer’s bank

- Beneficiary bank (the bank where the fraud amount was transferred)

The contribution depends on the size of the loss.

Case 1: Loss Less Than ₹29,412

If the loss amount is less than ₹29,412 and compensation of 85% of the loss is paid:

- 65% of the compensation will be paid by the RBI

- 10% by the customer’s bank

- 10% by the beneficiary bank

Case 2: Loss Between ₹29,412 and ₹50,000

If the loss is ₹29,412 or more but not more than ₹50,000, the compensation will be ₹25,000. In this case, the contribution will be fixed as follows:

- RBI: ₹19,118

- Customer’s bank: ₹2,941

- Beneficiary bank: ₹2,941

What Happens if Money Is Recovered Later

Sometimes banks may recover part of the fraud amount after compensation has already been paid. In such cases, the bank will recalculate the compensation based on the final net loss and adjust the amount accordingly.

Examples to Understand the Rule

Example 1: Recovery Before Compensation

- Total fraud loss: ₹40,000

- Recovery before compensation: ₹15,000

- Net loss: ₹25,000

Compensation paid (85% of ₹25,000): ₹21,250

Contribution:

- RBI: ₹16,250

- Customer’s bank: ₹2,500

- Beneficiary bank: ₹2,500

Example 2: Full Recovery After Compensation

- Reported loss: ₹40,000

- Compensation paid: ₹25,000

Contribution:

- RBI: ₹19,118

- Customer’s bank: ₹2,941

- Beneficiary bank: ₹2,941

Later, the entire ₹40,000 is recovered. The recovered amount will be distributed as:

- Customer: ₹15,000

- RBI: ₹19,118

- Customer’s bank: ₹2,941

- Beneficiary bank: ₹2,941

Example 3: Partial Recovery After Compensation

- Reported loss: ₹40,000

- Compensation paid: ₹25,000

Contribution:

- RBI: ₹19,118

- Customer’s bank: ₹2,941

- Beneficiary bank: ₹2,941

Later recovery: ₹15,000

Net loss becomes ₹25,000, so the correct compensation should be ₹21,250.

Additional payment calculation:

₹15,000 + ₹21,250 − ₹25,000 = ₹11,250

Distribution of recovery:

- Customer: ₹11,250

- RBI: ₹2,868

- Customer’s bank: ₹441

- Beneficiary bank: ₹441

Application Process for Compensation

After reviewing the complaint, if the bank believes that the fraud case is genuine, it will provide the customer with an application form.

Once the customer submits the application, the bank must pay the compensation within five calendar days.

Banks will later seek reimbursement of the applicable amount from the RBI on a quarterly basis.

Validity of the Compensation Scheme

The compensation will be available only for fraudulent electronic banking transactions that occur within one year from the effective date of these directions.

Click here to download RBI Circular