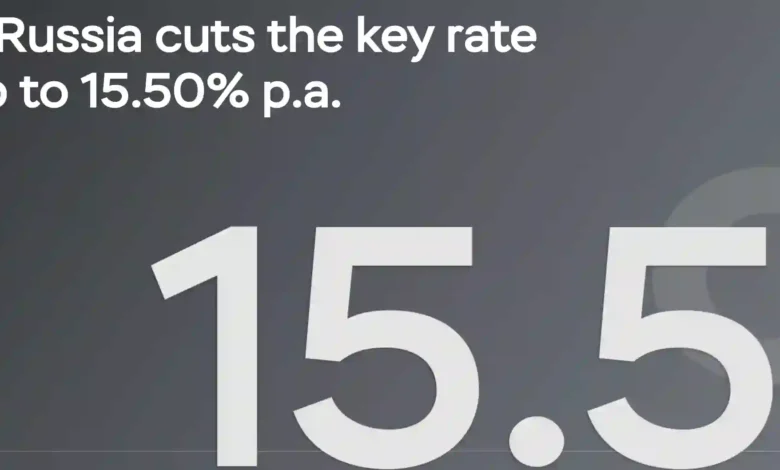

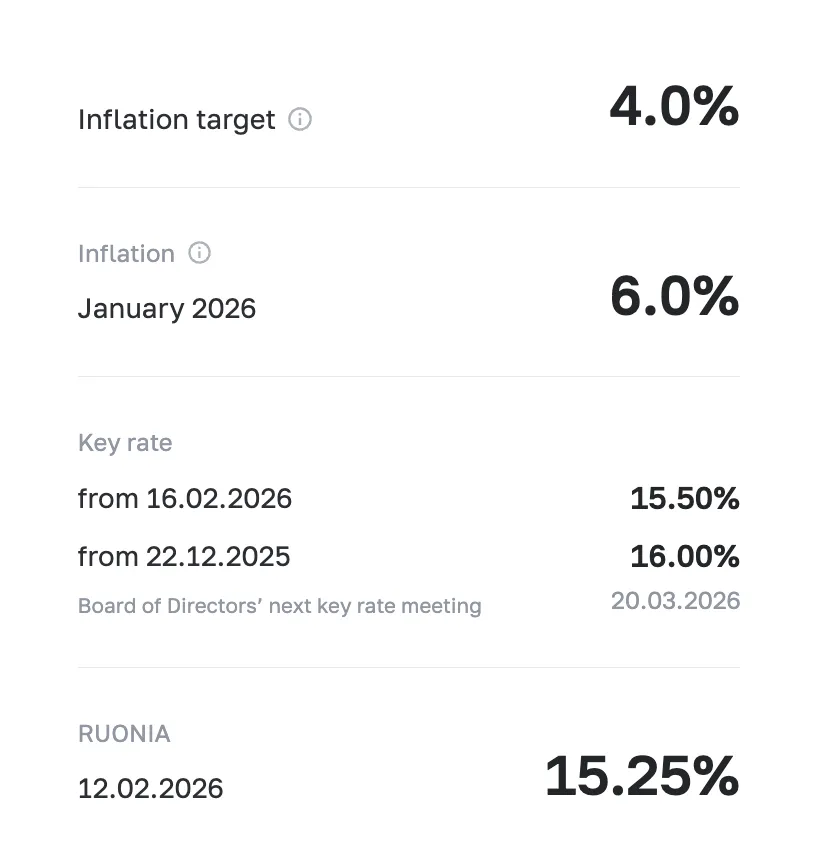

Russia has reduced its key interest rate by 0.50% (50 basis points). The new rate is now 15.50% per year.The Bank of Russia will decide in its future meetings whether to reduce the rate further. This decision will depend on how steadily inflation is falling and how people expect prices to move in the future.

In its base forecast, the Bank expects the average key rate to remain between 13.5% and 14.5% in 2026. This means monetary policy will still be strict, and borrowing costs will remain high. According to the Bank’s forecast, because of its current policy, annual inflation is expected to fall to 4.5%–5.5% in 2026.

Core (underlying) inflation is likely to be around 4% in the second half of 2026. From 2027 onwards, inflation is expected to remain at the target level.

Highlights of Meeting

In the fourth quarter (Q4) of 2025, price growth slowed down. The average seasonally adjusted price growth was 3.9% per year, compared to 6.5% in the third quarter (Q3) of 2025. Core inflation, which excludes volatile items, was 4.7% in Q4, slightly higher than 4.1% in the previous quarter. In recent months, most underlying inflation indicators remained between 4% and 5% on an annual basis. As of 9 February 2026, annual inflation stood at 6.3%.

At the end of 2025, prices of several goods, especially fruits and vegetables, showed very low growth. Also, the increase in VAT was not fully reflected in prices in December. Because of this, inflation at the end of 2025 was lower than the Bank of Russia had expected in October, reaching 5.6%. However, at the beginning of 2026, the situation changed. Higher VAT and excise taxes, increases in regulated prices and tariffs, and price adjustments for fruits and vegetables caused a temporary but sharp rise in prices in January.

As a result, some inflation that could have appeared in late 2025 shifted to early 2026. Overall, total price growth from November to January was in line with the Bank of Russia’s expectations. Underlying inflation is expected to fall to 4% in the second half of 2026. However, because of the shift in price growth to early 2026, the inflation forecast for 2026 has been raised to 4.5–5.5%.

Inflation expectations remain high. This may slow down the process of reducing inflation in a stable way.

The Russian economy is slowly returning to a more balanced growth path. For the full year 2025, GDP growth reached 1.0%, which was at the upper end of the Bank’s October forecast range. Although overall economic growth slowed during the year, it picked up in Q4 2025 due to stronger consumer demand. This may have been partly driven by expectations of higher VAT and recycling fees. Domestic demand is expected to slow in the coming months. Business surveys also show similar expectations.

The labour market is gradually becoming less tight. Surveys show that the number of companies facing labour shortages has fallen to its lowest level since mid-2023. Companies are planning smaller wage increases in 2026 compared to the period from 2023 to 2025. However, unemployment remains very low, and wages are still growing faster than labour productivity.

Monetary conditions have become slightly easier but remain tight. Loan and deposit interest rates have declined after earlier policy easing. Money market rates and government bond yields increased but stayed mostly stable after adjusting for inflation. Banks are still maintaining strict lending standards.

Loan growth slowed between late 2025 and early 2026 after faster growth in the autumn months. Households are continuing to save a large part of their income.

In the medium term, risks of higher inflation remain stronger than risks of lower inflation. The main risks include the economy staying above its balanced growth level for too long, high inflation expectations, the impact of higher VAT and regulated prices, and weaker external trade conditions. A slowdown in the global economy, rising trade disputes, and low oil prices could weaken the ruble and increase inflation. Geopolitical tensions also remain an important source of uncertainty. On the other hand, inflation could fall faster if domestic demand slows more than expected.

The Bank of Russia has taken into account the announced fiscal policy plans. In the medium term, fiscal policy is expected to support the reduction of inflation. However, any changes in fiscal policy may require adjustments in monetary policy.