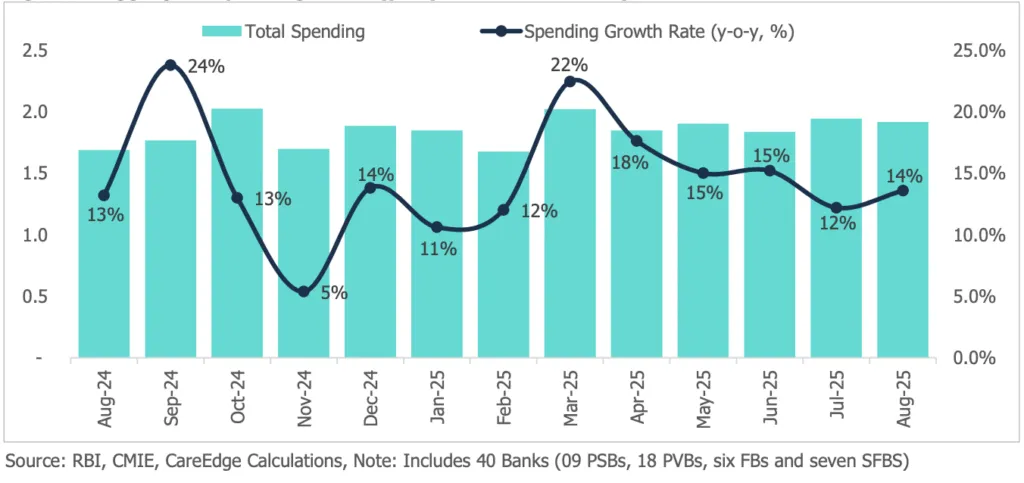

India’s credit card spending increased 14% in August 2025 compared to last year, reaching $21.1 billion (₹1.92 lakh crore). The increase came from higher incomes, more people using credit cards, and the growing popularity of digital payments, according to CareEdge Ratings.

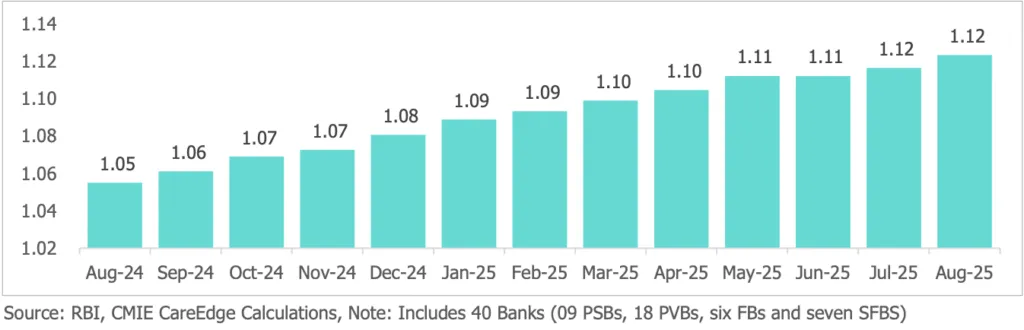

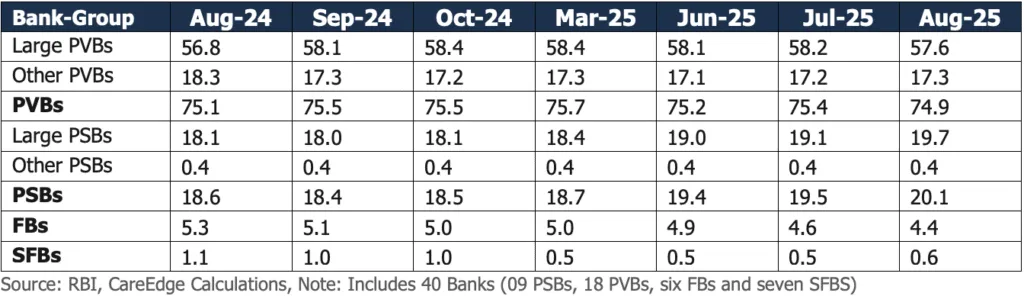

Private banks led the way, making up about 75% of total spending, though their share fell a little from last year. Public sector banks improved their share to around 20%. On average, each cardholder spent $191.8 (₹17,432), which is 6.7% higher than a year ago. The total number of credit cards in use increased from 1.05 crore in August 2024 to 1.12 crore in August 2025, showing steady growth in the use of credit cards.

In August 2025, people using private sector bank (PVB) cards spent an average of ₹19,717 per card, which is 5.8% higher than last year. This was more than public sector bank (PSB) cardholders, who spent an average of ₹14,253 per card. The total outstanding credit card balance increased 4.4% year-on-year to $31.8 billion (₹2.89 lakh crore).

Aggregate Spending Trend (y-o-y %, ₹ Lakh Crores)

No of Credit Cards Outstanding Increase y-o-y ( Fig. in crore)

The total number of credit cards in use increased from 1.05 crore in August 2024 to 1.12 crore in August 2025, showing a 6.5% year-on-year growth. Private banks continue to lead the credit card market, holding a 74.9% share in total spending as of August 2025. However, this is slightly lower than 75.1% a year earlier, mainly due to changes among large private banks. In comparison, public sector banks (PSBs) have a smaller presence, with around 20% of the total spending, mostly from a few large PSBs. The smaller PSBs play only a minor role, accounting for just about 0.5% of total credit card spending.

The market share of banks is as given below:

In August 2025, people using private sector bank (PVB) credit cards spent an average of ₹19,717 per card, which is 5.8% higher than last year. This was more than public sector bank (PSB) users, who spent an average of ₹14,253 per card. The higher spending among private banks is mainly because they serve urban, high-income customers who have larger credit limits. Their better reward programs, partnerships with e-commerce platforms, and strong digital services also encourage higher spending. Overall, average spending per card was ₹17,432 in August 2025, which is 0.8% lower than July 2025 (₹17,581) but 6.7% higher than August 2024 (₹16,153). The small month-on-month decline shows that spending has returned to normal after strong activity in July, which was boosted by end-of-season sales and early festive offers.

The total outstanding credit card balances stood at ₹2.89 lakh crore as of August 2025, compared to ₹2.91 lakh crore in July 2025 and ₹2.76 lakh crore in August 2024, indicating a moderate y-o-y growth of 4.4%.

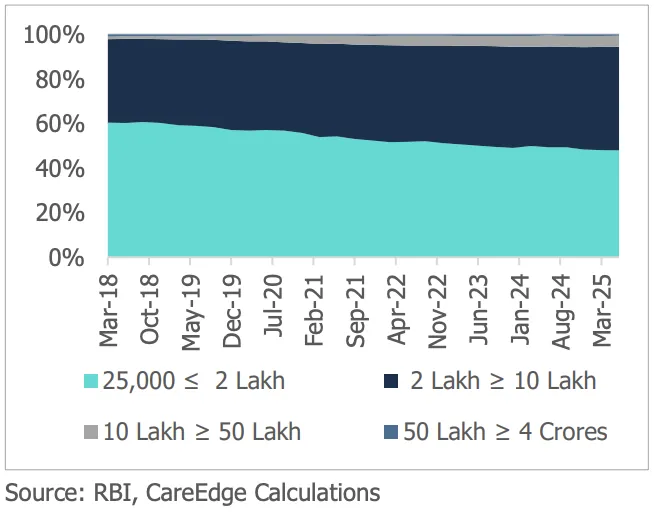

Limit Wise Credit Cards

Credit cards with limits between ₹25,000 and ₹2 lakh make up more than half of the market, holding the largest share of both credit limits and outstanding balances. This category has more than 50% market share. This means that maximum number of credit cards are issued in range of Rs.25,000 to Rs.2 Lakh.

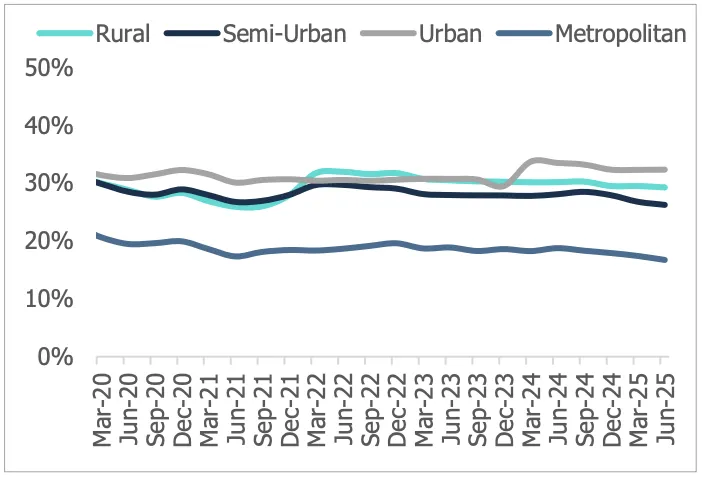

Credit Card use in Rural, Semi-Urban, Urban and Metro Regions

Now, if we talk about credit card usage in urban, semi-urban, rural and metro areas then the maximum usage of credit cards is in Metro areas. As of June 2025, total credit limits were:

- Metros: ₹11,60,311 crore

- Urban areas: ₹1,39,349 crore

- Semi-urban areas: ₹86,480 crore

- Rural areas: ₹21,705 crore

The corresponding credit used (utilisation) was:

- Metros: ₹1,93,501 crore

- Urban areas: ₹44,945 crore

- Semi-urban areas: ₹22,636 crore

- Rural areas: ₹6,335 crore

Metros and urban areas still lead in total credit use. However, the utilisation ratios across all regions have slightly declined, showing lower discretionary spending and tighter credit management due to rising unsecured loan risks. At the same time, rural and urban areas have shown stable credit use, indicating that essential spending continues steadily.

Download Report PDF (This PDF is available for Premium Users Only. Click here to join premium)

-

-

-

-

-

-

-

![RBI released Bulletin December 2025 [Download PDF]](https://hellobanker.in/wp-content/uploads/2025/12/Orange-and-White-Geometric-Food-Vlogger-YouTube-Channel-Art-1-390x220.webp)

-

-

-

-

![Deposit and Credit Data of Scheduled Commercial Banks [PDF]](https://hellobanker.in/wp-content/uploads/2025/12/Deposit-and-Credit-Data-of-Scheduled-Commercial-Banks-PDF-390x220.webp)

-