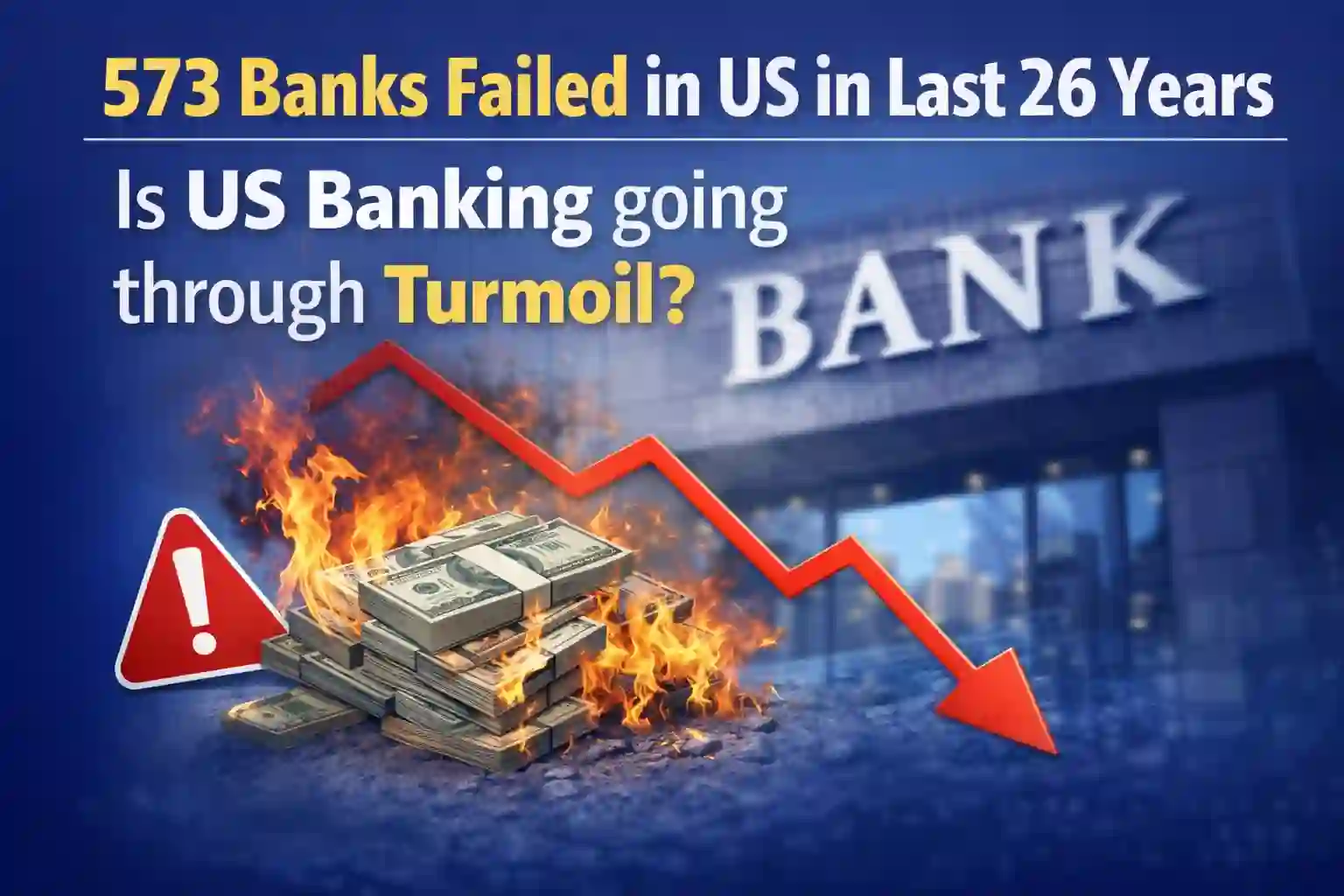

Did You Know? 573 banks have failed in the USA in the last 26 years (from 2000 till January 2026). The largest economy in the World is going through a big turmoil in the banking industry. 573 is a large number and has raised a serious concern about the banking system in the USA. The latest bank to fail is Metropolitan Capital Bank & Trust, which was closed on 30th January 2026. The banks were closed due to concerns over their financial stability.

The details of the failed banks since 2020 are given below:

| Bank Name | City | Acquiring Institution | Closing Date |

|---|---|---|---|

| Metropolitan Capital Bank & Trust | Chicago | First Independence Bank | 30-Jan-26 |

| The Santa Anna National Bank | Santa Anna | Coleman County State Bank | 27-Jun-25 |

| Pulaski Savings Bank | Chicago | Millennium Bank | 17-Jan-25 |

| First National Bank of Lindsay | Lindsay | First Bank & Trust Co. | 18-Oct-24 |

| Republic First Bank dba Republic Bank | Philadelphia | Fulton Bank, National Association | 26-Apr-24 |

| Citizens Bank | Sac City | Iowa Trust & Savings Bank | 3-Nov-23 |

| Heartland Tri-State Bank | Elkhart | Dream First Bank, N.A. | 28-Jul-23 |

| First Republic Bank | San Francisco | JPMorgan Chase Bank, N.A. | 1-May-23 |

| Signature Bank | New York | Flagstar Bank, N.A. | 12-Mar-23 |

| Silicon Valley Bank | Santa Clara | First–Citizens Bank & Trust Company | 10-Mar-23 |

| Almena State Bank | Almena | Equity Bank | 23-Oct-20 |

| First City Bank of Florida | Fort Walton Beach | United Fidelity Bank, fsb | 16-Oct-20 |

| The First State Bank | Barboursville | MVB Bank, Inc. | 3-Apr-20 |

| Ericson State Bank | Ericson | Farmers and Merchants Bank | 14-Feb-20 |

Complete List of Failed Banks in USA since 2000

Also Read: Goldman Sachs CEO Gets 21% Pay Hike in 2025, Check His Salary

Why Are Banks Failing in the US?

Banks in the United States have failed mainly due to a combination of economic pressure, weak risk management, and a sudden loss of customer confidence. One of the biggest reasons has been the sharp rise in interest rates. To control high inflation, the US Federal Reserve increased interest rates rapidly. As a result, banks that had invested heavily in long-term bonds suffered major losses because bond prices fall when interest rates rise. These losses weakened bank balance sheets and reduced their financial strength.

Another major factor has been bank runs and loss of confidence. When customers fear that a bank may collapse, they rush to withdraw their money. Even a financially sound bank can fail if too many depositors withdraw funds at the same time. In recent years, social media and digital banking have made such withdrawals faster than ever, worsening liquidity problems for banks.

Also Read: Big Legal Battle between Trump and Largest US Bank! JPMorgan Closed Accounts of US President

High exposure to risky sectors has also played a key role. Some failed banks were heavily dependent on deposits from tech startups, crypto firms, and venture capital-backed companies. When these sectors slowed down due to higher interest rates and weaker funding conditions, deposits fell sharply, putting additional pressure on banks.

Poor risk management further increased vulnerabilities. Many banks failed to properly hedge interest rate risk, maintain sufficient liquid assets, or diversify their loan and deposit base. This lack of preparation made them highly exposed during periods of economic stress.

Also Read: US imposes Lifetime Ban on Bank Loan Officer for Mortgage Fraud

Stress in the commercial real estate sector has also hurt banks, especially mid-sized and regional lenders. Rising interest rates and work-from-home trends reduced demand for office buildings and retail spaces. As a result, loan defaults increased, weakening bank balance sheets.

Regulatory gaps have been another concern. Some mid-sized banks were subject to lighter regulations compared to large banks. Reduced stress testing and looser oversight allowed higher risk-taking, which increased the chances of failure during economic shocks.

Also Read: US plans to impose Cap on credit card interest rates, Banks can’t charge more than 10%

Historical crises have also contributed significantly to the total number of bank failures. Many of the 573 bank failures over the past 26 years occurred during the 2008 Global Financial Crisis and the COVID-19 economic shock. These periods caused widespread loan defaults, sharp economic slowdowns, and severe liquidity stress across the banking system.

Is the US Banking System in Crisis?

The US banking system is not facing a full-scale crisis, but stress remains, particularly among small and mid-sized banks. Large US banks are generally well-capitalised and better regulated. However, confidence issues and liquidity risks continue to be key concerns.

-

-

-

-

-

-

-

-

-

-

-

-